When it comes to building long-term wealth, investors often find themselves asking — ETF vs Mutual Fund: which is better? Both are excellent tools for diversification and compounding, but their structure, cost, and management style can make a big difference in returns over time.

In this detailed guide, we’ll explain the key differences between ETFs and mutual funds, explore their pros and cons, and help you understand which investment might suit your financial goals better — especially from the perspective of Indian investors.

📘 What is an ETF? (ETF Explained)

An ETF (Exchange-Traded Fund) is an investment fund that holds a basket of securities — like stocks, bonds, or commodities — and trades on the stock exchange just like individual shares.

ETFs are designed to track an index, such as the Nifty 50, Sensex, or even the S&P 500 ETF in global markets.

For example:

- A Nippon India Nifty 50 BeES ETF tracks the Nifty 50 Index.

- A Gold ETF mirrors the price of gold.

- A Global ETF may track international indices like NYSEARCA VOO, NYSEARCA VGT, or NYSEARCA VTI.

Unlike mutual funds, ETF prices fluctuate throughout the day as they are traded on exchanges, offering higher liquidity and transparency.

👉 You can learn more about ETFs in our detailed guide — What is an ETF? A Beginner’s Guide for Indian Investors

🏦 What is a Mutual Fund?

A mutual fund pools money from many investors and invests it in a mix of securities — equities, bonds, or money market instruments — based on the fund’s objective.

Mutual funds are usually actively managed by professional fund managers who try to outperform benchmarks.

Investors buy or sell mutual fund units at the end of the day’s NAV (Net Asset Value), unlike ETFs that can be traded anytime during market hours.

Mutual funds are ideal for investors looking for convenience, SIP options, and expert management without having to monitor markets daily.

⚖️ ETF vs Mutual Fund: Key Differences

| Feature | ETF (Exchange-Traded Fund) | Mutual Fund |

|---|---|---|

| Management | Mostly Passive (tracks an index) | Actively or passively managed |

| Trading | Buy/sell anytime during market hours | Buy/sell once daily at NAV |

| Costs | Low expense ratio, minimal management fees | Higher expense ratio |

| Transparency | Daily holdings disclosed | Monthly or quarterly holdings |

| Liquidity | High (exchange-traded) | Lower (processed via AMC) |

| Minimum Investment | 1 unit | ₹500 (via SIP) |

| Taxation | Similar to equity or debt mutual funds | Similar structure |

| Best for | Cost-conscious, long-term investors | SIP investors or beginners |

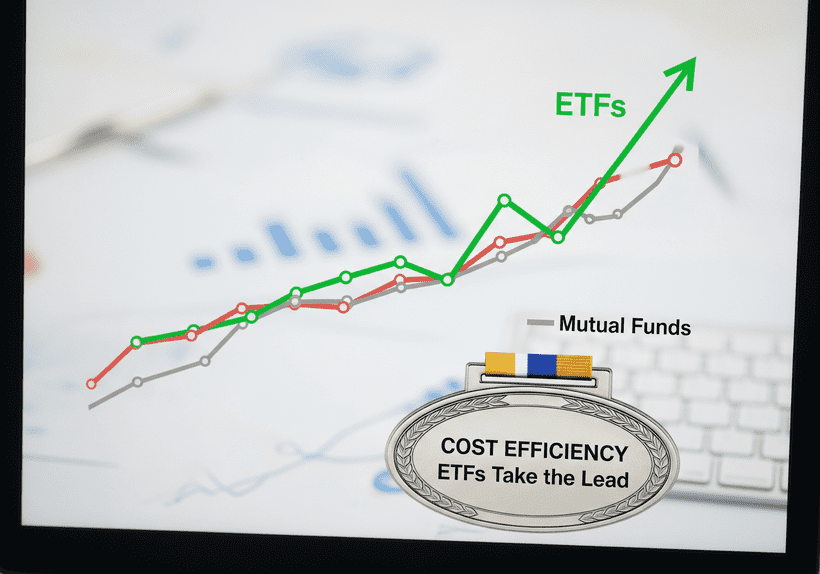

💰 Cost Efficiency: ETFs Take the Lead

One of the biggest advantages of ETFs over mutual funds is cost.

ETFs have much lower expense ratios because they’re passively managed, tracking an index rather than paying fund managers to pick stocks.

For example:

- Average Nifty 50 ETF expense ratio: 0.05% to 0.3%

- Average active mutual fund expense ratio: 1% to 2.25%

Over 15–20 years, these cost differences can significantly impact returns.

Even a 1% lower expense ratio can mean ₹3–4 lakh more wealth for long-term SIP investors.

Learn more about how expense ratios affect your investments in our post — Importance of Expense Ratio in Mutual Fund Returns

📈 Tax Efficiency: ETF vs Mutual Fund in India

When it comes to taxation, both ETFs and mutual funds are treated similarly under Indian tax laws.

- Equity ETFs and equity mutual funds:

- Short-Term Capital Gains (STCG) – 15% (if sold within 1 year)

- Long-Term Capital Gains (LTCG) – 10% above ₹1 lakh (after 1 year)

- Debt ETFs and debt mutual funds:

- Taxed as per investor’s income slab (post-April 2023 changes).

However, ETFs are more tax-efficient in structure, especially globally, because they rely on “in-kind” transfers instead of triggering internal capital gains through fund redemptions.

In simple terms, ETFs help you defer tax longer, allowing your investment to compound better.

💹 Liquidity & Flexibility: ETFs Provide More Control

ETFs are traded like stocks on the NSE and BSE, meaning investors can buy or sell them anytime during market hours at live prices.

This provides:

- Real-time control over transactions

- Transparency in pricing

- No exit loads (unlike some mutual funds)

Mutual funds, on the other hand, are valued at the end-of-day NAV, and orders are executed at that day’s closing price.

However, mutual funds offer SIP (Systematic Investment Plan) options, which many investors prefer for disciplined long-term investing.

If you’re new to SIPs, check out our beginner’s guide — Step-by-Step Guide: How to Start SIP

🧩 Diversification and Accessibility

Both ETFs and mutual funds provide diversification, but ETFs can go beyond domestic markets.

You can invest in:

- Gold ETF for commodity exposure

- Global ETF for international markets (like S&P 500 ETF, NASDAQ 100 ETF)

- Sectoral ETFs like Tech ETF or Financial ETF

- Government ETFs like Bharat Bond ETF

This allows investors to build an ETF portfolio across asset classes — equities, commodities, bonds, and even crypto ETFs (for global markets).

Mutual funds also provide diversification but are typically limited to Indian assets.

🌍 Global Exposure Through ETFs

ETFs offer seamless global diversification. Indian investors can access:

- NYSEARCA VOO – S&P 500 ETF

- NYSEARCA VGT – Tech Growth ETF

- NYSEARCA VWO – Emerging Markets ETF

- NYSEARCA VIG – Dividend Growth ETF

- NYSEARCA UYG – Financial ETF

These ETFs give exposure to the U.S. markets, technology sector, and global economic growth, which traditional Indian mutual funds may not cover.

🧠 Performance Over the Long Term

Data shows that passive ETFs often outperform active mutual funds over 10–15 years due to lower costs and consistent index tracking.

In India, Nifty and Sensex ETFs have matched or exceeded the performance of many large-cap funds.

However, active mutual funds can still outperform in mid-cap or thematic categories, where fund managers can identify emerging opportunities before they’re widely recognized.

Thus, for long-term wealth creation, ETFs offer consistency, while mutual funds offer potential outperformance (at a higher cost).

🔧 Building a Long-Term ETF and Mutual Fund Portfolio

A well-structured portfolio can include both:

Example: Balanced Wealth Creation Portfolio (India, 2025)

- 40% Index ETF (like Nippon Nifty 50 BeES or SBI ETF Sensex)

- 20% Gold ETF (stability & inflation hedge)

- 20% Global ETF (diversification to S&P 500 or NASDAQ 100)

- 20% Active Mutual Funds (mid-cap or flexi-cap)

This hybrid approach captures the best of both worlds — low-cost, diversified ETFs for stability and select mutual funds for growth potential.

⚠️ Risks and Limitations

While ETFs offer many advantages, there are a few risks:

- Tracking Error: ETF performance may deviate slightly from the index.

- Liquidity Risk: Some ETFs have low trading volumes in India.

- Market Volatility: ETF prices fluctuate with the market.

Mutual funds carry manager risk, exit loads, and higher expense ratios, which may reduce net returns.

Always assess your risk appetite and time horizon before deciding between ETF vs mutual fund.

💬 Our Role as a Mutual Fund Distributor

We are a registered mutual fund distributor, dedicated to guiding investors in making informed financial decisions. While we share insights on ETFs and global investing, our primary focus is helping clients build strong mutual fund and SIP portfolios that align with their long-term wealth goals.

❓ FAQs: ETF vs Mutual Fund in India

1. Which is better for long-term wealth creation — ETF or mutual fund?

ETFs usually outperform due to lower costs and stable returns, but mutual funds may deliver better results in certain active categories.

2. Can I start SIP in ETFs?

Yes, some platforms allow SIP-style investing in ETFs through periodic purchases.

3. Is ETF safer than mutual fund?

Both are market-linked. ETFs are more transparent, while mutual funds offer professional management.

4. Which has lower cost — ETF or mutual fund?

ETFs generally have much lower expense ratios, making them cost-effective for long-term investors.

5. Are ETFs tax-free in India?

No, ETFs are taxed similarly to mutual funds under equity or debt categories.

🧾 Conclusion

The ETF vs Mutual Fund debate isn’t about which is absolutely better — it’s about which suits your investment style.

- Choose ETFs if you prefer low costs, transparency, and global diversification.

- Choose mutual funds if you value SIP convenience and professional management.

For most Indian investors, a hybrid portfolio combining both ETFs and mutual funds can be the best strategy for long-term wealth creation.

⚠️ Disclaimer

This article is for educational purposes only and should not be taken as investment advice. Past performance does not guarantee future results. Always assess your risk tolerance and consult a SEBI-registered financial advisor before investing in any ETF, mutual fund, or related product.