When it comes to investing, two of the most common options for Indian investors are mutual funds and fixed deposits (FDs). Both are popular, widely available, and suitable for different types of investors. But the question that often comes up is: mutual fund vs fixed deposit – which is better?

The answer isn’t the same for everyone. The choice depends on your risk tolerance, financial goals, liquidity needs, and tax preferences. In this detailed guide, we will break down the difference between mutual fund and fixed deposit, analyze mutual fund vs FD returns, explore tax benefits, compare risks, and ultimately help you decide which is better: mutual fund or fixed deposit.

What is a Fixed Deposit (FD)?

A Fixed Deposit (FD) is a traditional savings instrument offered by banks and financial institutions. Investors deposit a lump sum for a fixed tenure and receive guaranteed interest. FDs are considered extremely safe because they are not market-linked, and deposits are insured up to ₹5 lakh under the Deposit Insurance and Credit Guarantee Corporation (DICGC).

Key features of FDs:

- Guaranteed, fixed returns (usually 5%–7% per annum)

- Safe and risk-free investment

- Fixed tenure ranging from 7 days to 10 years

- Premature withdrawals allowed with penalty

- Interest taxed as per investor’s income slab

FDs are ideal for conservative investors, retirees, or anyone looking for guaranteed income without worrying about market fluctuations.

What is a Mutual Fund?

A Mutual Fund pools money from multiple investors and invests in a diversified portfolio of equities, bonds, or hybrid instruments. They are managed by professional fund managers, and returns depend on market performance.

Key features of Mutual Funds:

- Market-linked returns (10%–15% average for equity funds in long term)

- Wide range of options: equity, debt, hybrid, liquid, and ELSS funds

- Flexible investment amounts through SIPs (Systematic Investment Plans)

- Higher risk compared to FDs but also higher growth potential

- Tax benefits available under ELSS (Equity Linked Savings Scheme)

Mutual funds are suited for investors who want to build wealth, beat inflation, and are willing to accept some level of market risk.

Difference Between Mutual Fund and Fixed Deposit

The most important difference between mutual fund and fixed deposit is that FDs provide fixed, guaranteed returns, while mutual funds offer variable, market-linked returns.

Here are the main distinctions:

| Factor | Fixed Deposit (FD) | Mutual Fund |

|---|---|---|

| Returns | Fixed (5–7%) | Market-linked (could be higher or lower) |

| Risk | Almost zero | Varies (low for debt funds, high for equity funds) |

| Liquidity | Premature withdrawal penalty | Can redeem anytime (except ELSS lock-in) |

| Taxation | Interest is fully taxable as per the slab | ELSS funds are eligible for 80C deduction; capital gains are taxed separately |

| Investment Mode | Lump sum | Lump sum or SIP (monthly) |

| Suitability | Conservative investors, retirees | Investors seeking long-term wealth |

FDs are safe, but mutual funds provide better opportunities for long-term capital appreciation.

Mutual Fund vs FD Returns

When analyzing mutual fund vs FD returns, it’s clear that mutual funds usually outperform FDs in the long run.

- Fixed Deposits: Offer 5%–7% annual returns. Senior citizens may get slightly higher rates. However, FD returns often fail to beat inflation.

- Mutual Funds:

- Equity mutual funds: 10%–15% annualized returns over long term

- Debt mutual funds: 6%–9% returns, with lower risk

- Hybrid funds: Balanced risk, 8%–12% returns

While FDs guarantee safety, they don’t generate wealth as effectively as mutual funds. Investors seeking higher growth prefer mutual funds, despite the risks.

Mutual Fund vs Fixed Deposit Tax Benefits

Taxation is another crucial factor in the mutual fund vs fixed deposit tax benefits debate.

- Fixed Deposits:

- Interest earned is fully taxable as per your income slab.

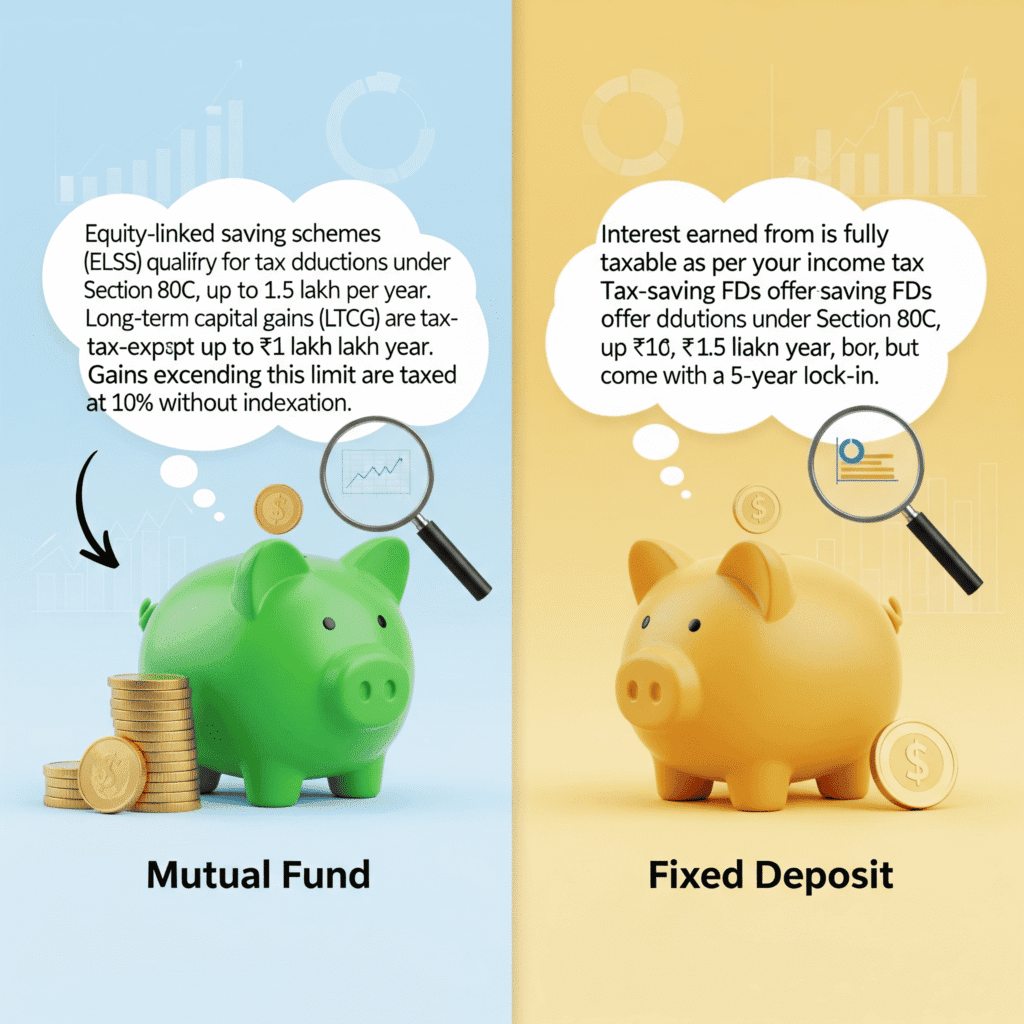

- No exemptions except tax-saving 5-year FDs under Section 80C (₹1.5 lakh limit).

- Mutual Funds:

- ELSS (Equity Linked Savings Scheme) qualifies for Section 80C benefits up to ₹1.5 lakh.

- Long-term capital gains (LTCG) above ₹1 lakh on equity funds taxed at 10%.

- Short-term capital gains (STCG) taxed at 15%.

- Debt funds taxed differently (linked to income slab and capital gains rules).

Thus, mutual funds can provide better tax efficiency, especially through ELSS.

Fixed Deposit vs Mutual Fund Risk Comparison

When it comes to fixed deposit vs mutual fund risk comparison, FDs are clearly the safer choice.

- Fixed Deposits:

- Virtually risk-free

- Covered by insurance (up to ₹5 lakh per depositor per bank)

- Returns guaranteed

- Mutual Funds:

- Carry market risk, interest rate risk, and liquidity risk

- Different types have different risk profiles (equity = high risk, debt = low risk)

- Returns are not guaranteed

Risk-averse investors should prioritize FDs, while those willing to take moderate risk for higher returns can go for mutual funds.

Which is Better – Mutual Fund or Fixed Deposit?

If you are wondering which is better mutual fund or fixed deposit, the answer lies in your financial goals:

- Choose Fixed Deposits if you want:

- Guaranteed returns

- Safety and capital protection

- Short-term investment option

- No market dependency

- Choose Mutual Funds if you want:

- Higher long-term returns

- Inflation-beating investments

- Tax efficiency through ELSS

- Diversification and wealth creation

Most financial advisors recommend having a balance of both—FDs for safety and stability, and mutual funds for long-term growth.

Real-Life Examples

- Case 1 – Retired Investor:

Mr. Sharma, a retired professional, prefers FDs for steady income. He cannot afford risks, so he allocates 80% to FDs and only 20% to debt mutual funds for slightly better returns. - Case 2 – Young Professional:

Riya, a 28-year-old IT professional, invests primarily in mutual funds via SIPs. She has a long-term horizon and higher risk appetite, so mutual funds suit her better than FDs.

Quick Comparison Table

| Factor | Fixed Deposit (FD) | Mutual Fund |

|---|---|---|

| Returns | 5–7% fixed | 10–15% equity (long term) |

| Risk | Almost zero | Moderate to high |

| Liquidity | Penalty on premature withdrawal | Redeem anytime (except ELSS) |

| Tax Benefits | Limited (only tax-saving FD) | ELSS under 80C, LTCG rules |

| Investor Type | Retirees, conservative | Young, growth-oriented |

Conclusion

The debate of mutual fund vs fixed deposit ultimately comes down to personal preference. If your priority is safety, stability, and guaranteed returns, FDs are a reliable choice. However, if your goal is wealth creation, higher returns, and long-term growth, mutual funds outperform FDs despite carrying risks.

A balanced approach—where you secure part of your savings in FDs while allocating a portion to mutual funds—can give you both security and growth.

So, before making a decision, carefully assess your risk appetite, investment horizon, and tax situation. That will determine which is better: mutual fund or fixed deposit for you.

-

- What is an IPO? A Beginner’s Guide

- Upcoming IPOs in India

- Top Benefits of Investing in Mutual Funds for Beginners

- Top Mistakes Retail Investors Make