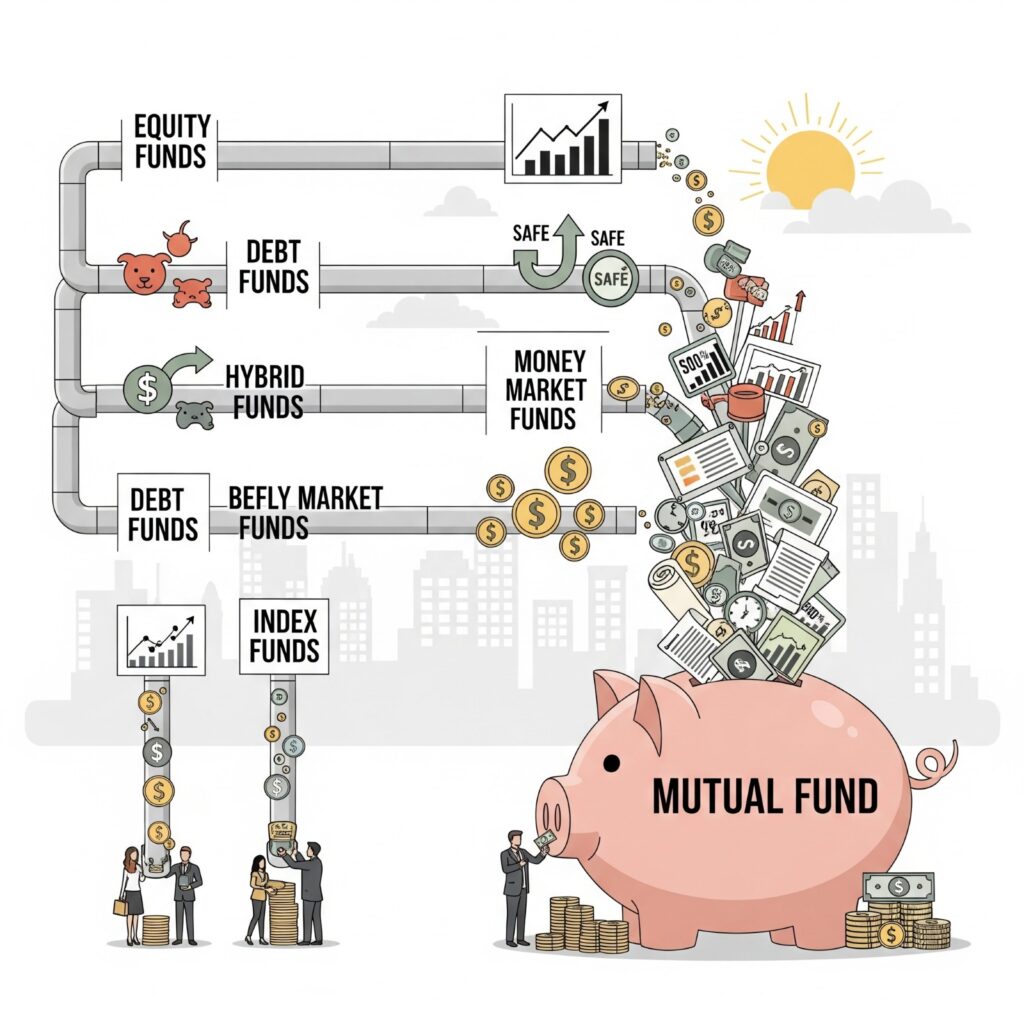

A mutual fund is a type of investment that collects money from many investors and pools it together into a single fund. This money is then managed by professional fund managers, whose primary job is to invest it across different types of financial instruments like stocks, bonds, gold, government securities, or assets, depending on the type of mutual fund.

Think of a mutual fund as a basket of investments. Instead of buying individual company shares on your own, you contribute your money to a common pool. The fund manager then uses this pool to buy a wide variety of investments. This makes it possible for even small investors to access a diversified portfolio.

Mutual funds are not just for beginners; experienced investors also rely on them to grow wealth steadily, and also for long-term wealth creation, retirement planning, tax-saving, and achieving financial goals like buying a house, funding education or liabilities. With the flexibility to invest in lump sums or SIPs, mutual funds are suitable for both short-term and long-term investors.

For example :

You invest ₹10000 in a mutual fund. This money will be divided and invested in different bonds, gold, government securities, and different companies’ stock, like Reliance, HDFC Bank, Infosys, SBI, and others. If a company’s stock does not do well, then others are balanced to grow your money.

Why Should You Invest in Mutual Funds?

When you invest in a mutual fund, your money is collected together with other investors and managed by expert fund managers who carefully select stocks, bonds, gold, government securities, or assets. Investing in mutual funds is one of the smartest ways to grow your money because it offers diversification and is managed by professional people. This reduces the risk of your investments, protecting you from the ups and downs of any single company or sector. In simple terms, you get the benefit of owning a well-balanced portfolio without the stress of managing it yourself.

Advantages of Mutual Funds

1.Professional Management-

The investors’ money is managed by fund managers who are experts in analysing the stocks, bonds, gold, government securities, or other assets.

2.Diversification –

A mutual fund invests in many stocks, bonds, gold, government securities or other assets. So even if one stock does not perform well then others can balance the loss.

3.Liquidity-

The investors can buy and sell the mutual fund units easily on any business day.

4.Affordable Investment-

The investors can start investing with very small amounts. Some mutual funds can start with Rs.100.

5.Convenience-

In a mutual fund there is no need to track up and down of the market daily.The investors track can track the NAV ( Net Asset Value) of the mutual fund. There is an online platform that makes it easy to invest and monitor.

6.Regulation & Transparency-

SEBI ( Securities and Exchange Board of India) regulates the mutual fund of India. They ensure fair trade practices, investors protection and disclosures.

7.Tax Benefits-

ELSS (Equity Linked Savings Scheme) are offered tax benefits in mutual funds of India.Under the Section 80C of the Income tax Act.

Disadvantages of Mutual Funds

1.Costs / Fees-

Mutual Funds are charged Total expenses ratio and sometimes exit loads. Total expense ratio is Investment and advisory fees, Recurring Expenses like transaction cost, custodian fees and others.

2. Market Risk-

Most of the Mutual Funds are invested in the stock market that is why they are not risk free. If the market falls, investors’ investment value goes down.

3.No Control Over Portfolio-

The mutual Funds fund managers are deciding where to invest which stocks and bonds are selected to invest. So investors do not have control over their portfolio.

4.Return Not Guaranteed-

Mutual Funds are invested in Stock, Bonds, Gold and other financial instruments. So that’s why their returns are not guaranteed like Fixed Deposits and PPF.

5.Over-Diversification-

Some mutual fund managers are invested in too many securities so the investors does not get high potential returns.

6.Tax on gains-

Mutual fund Investors earn profit through selling their NAV units they are taxable under income tax act. If investors sell their units less than 12 months they are considered under STCG (short term Capital Gain) and if more than 12 months they are considered under LTCG ( Long Term Capital Gain).

Types of Mutual Funds in India

Before investing, it is important to understand the different types of mutual funds available in India. Each type targets different investor goals, whether it is wealth creation, regular income, or tax savings. Mutual Funds have become a common investment type because they provide professional assistance and easy withdrawals

Let’s break down the types of mutual funds and categories available in India including the features and examples

1. Equity Mutual Funds

In the Equity Mutual Funds scheme around 90-95% Money is put in the stocks. As per the SEBI Mutual Fund Regulations, an equity mutual fund must invest at least 65% of the scheme in the equities and equities related instruments. In an Equity Mutual Fund investors don’t need to track share price daily or decide which stock to buy or sell. All this work is done by the Fund manager.You just need to invest money and track the fund performance from time to time

If you stay invested for a long term like 15-20 years, the chances of earning a better high return also compared to debt funds.

Around 40-50 stocks in Equity Mutual Funds Portfolio this number can vary. Also In equity mutual funds there are many types. Let’s break down the types of equity mutual funds.

2. Debt Mutual Funds

Debt Mutual Funds invest in fixed income instruments like Government bonds, Corporate bonds, Treasury bills, commercial papers and Money Market Instruments.

Risk Level for debt mutual funds is Low to Moderate. The returns are stable, not too high or low. Volatility is less in debt funds. The debt mutual fund is best for short term 1 to 5 years. In debt mutual funds if investors have stable income with low risk debt mutual funds are the best option. A debt mutual fund is a safer option than equity mutual fund.

Let’s break down the types of Debt Mutual Funds

3. Hybrid Mutual Fund-

A Hybrid Mutual Funds money invest in a mixture of equity market and debt instruments. The balance of equity and debt maintains your growth. Equity gives a higher return and potential to grow more. Debt gives a stable and low risk income. Hybrid Mutual Funds are not too risky like pure equity funds, and not too safe like pure debt funds.

The main Goal of Hybrid Mutual Fund is balance risk and return by combining the growth potential of equities with the stability of debt.

Let’s explore the various categories of Hybrid Mutual Funds.

4. Index Funds

Index Fund is also known as Exchange Traded Fund (ETF). The index fund replicates the stock market index like NIFTY50, SENSEX and NIFTY 500 others.

5. Tax Saving-

ELSS (Equity Linked Savings Scheme) are offered tax benefits in mutual funds of India.Under the Section 80C of the Income tax Act.

Equity Linked Savings Scheme (ELSS) is a tax-saving mutual fund that allows investors to save on income tax under Section 80C of the Income Tax Act while also creating long-term wealth through equity investments. It comes with the shortest lock-in period among tax-saving instruments, just three years making it more flexible compared to options like PPF or NSC. Since ELSS primarily invests in equities and equity-related securities, returns are market-linked and have the potential to be higher, though they also carry a level of risk. Investors can choose to invest either as a lump sum or through SIPs, making ELSS a popular choice for those seeking both tax benefits and long-term financial growth.