💡 Introduction: Making Your Investments Work for You

Have you ever wished for a way to get a monthly income from your mutual funds—without redeeming them all at once? That’s exactly what a Systematic Withdrawal Plan (SWP) does.

Think of an SWP like a salary from your investments. It allows you to withdraw a fixed amount from your mutual fund at regular intervals—monthly, quarterly, or annually—while the rest of your money stays invested and continues to grow.

In today’s market, where investors are looking for both growth and stability, understanding how an SWP works can be a game-changer.

Let’s explore how this powerful tool works, why it’s so popular among retirees and working professionals alike, and how Busyshell, through Omkar Mokashi, can help you use it smartly.

🧩 What is a Systematic Withdrawal Plan (SWP)?

A Systematic Withdrawal Plan (SWP) is a feature offered by mutual funds that allows investors to withdraw a fixed amount from their investments at regular intervals.

Instead of redeeming your full investment, you can schedule withdrawals—say ₹10,000 every month—while the remaining units continue to earn returns.

👉 Example:

Suppose you invest ₹10 lakh in a balanced mutual fund through Busyshell. You decide to start an SWP of ₹10,000 per month. Each month, the mutual fund redeems the required number of units based on that day’s NAV and credits ₹10,000 to your bank account.

If the NAV goes up, fewer units are sold; if the NAV falls, more units are redeemed. Meanwhile, the rest of your corpus remains invested—compounding and growing.

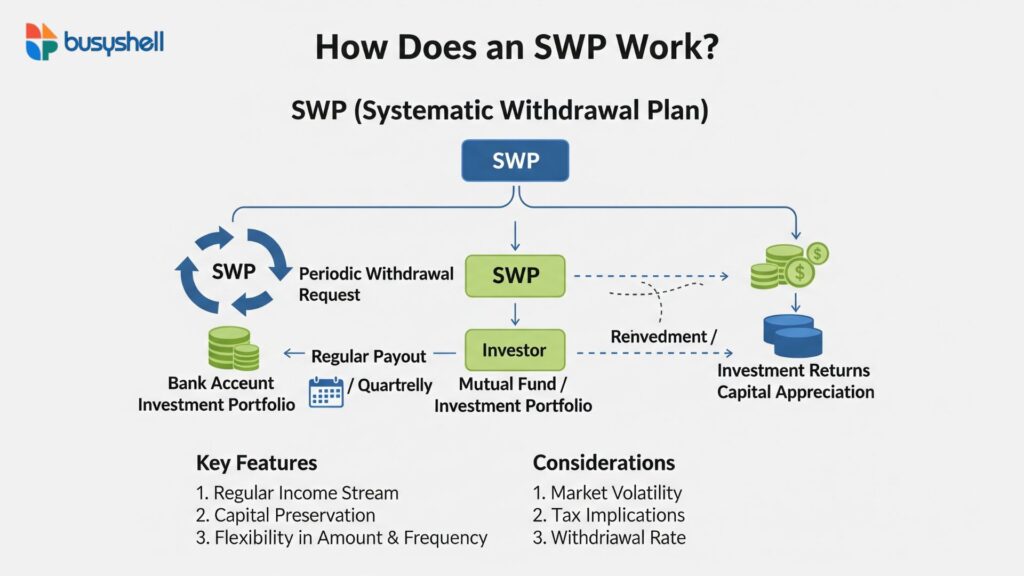

⚙️ How Does an SWP Work?

An SWP works like the opposite of an SIP (Systematic Investment Plan).

| Type | SIP | SWP |

|---|---|---|

| Direction | You invest regularly | You withdraw regularly |

| Goal | Wealth creation | Regular income |

| Suitable for | Accumulation phase | Withdrawal phase |

| Frequency | Monthly, quarterly, yearly | Monthly, quarterly, yearly |

Step-by-step example:

- Initial investment: ₹12,00,000 in an equity hybrid fund.

- Start SWP: ₹20,000 per month.

- Duration: 5 years.

- Assumed annualized return: 9%.

After 5 years, you would have received ₹12 lakh in withdrawals, and still have a corpus of around ₹7.5 lakh (approx.), assuming stable market performance.

That’s the power of Systematic Withdrawal Plans (SWPs)—steady income while keeping your capital invested.

📈 Why Investors Choose SWP over Lump-Sum Withdrawals

Here’s why Indian and global investors increasingly prefer Systematic Withdrawal Plans (SWPs):

- Regular cash flow: Ideal for retirees, freelancers, or anyone seeking monthly income.

- Rupee cost averaging (reverse): You sell fewer units when NAVs are high, protecting returns.

- Tax efficiency: Especially beneficial under the long-term capital gains (LTCG) regime.

- Market participation: Your remaining investment continues to grow.

- Flexibility: Start, stop, or modify your SWP anytime.

💰 Taxation of Systematic Withdrawal Plans (SWPs)

Taxation is where many investors get confused—so let’s break it down simply.

📊 1. Equity Mutual Funds

- If your units are sold within 12 months, the gain is Short-Term Capital Gain (STCG) and taxed at 15%.

- If sold after 12 months, gains above ₹1 lakh are Long-Term Capital Gains (LTCG) taxed at 10% (without indexation).

📊 2. Debt Mutual Funds

- Units sold before 36 months → STCG taxed as per your income tax slab.

- Units sold after 36 months → LTCG taxed at 20% with indexation (for investments made before April 2023).

- For investments after April 2023 (under new debt taxation rules), returns are taxed as per your slab rate.

🔹 In an SWP, each withdrawal consists of both principal and gain, so only the gain portion is taxable.

Example:

If ₹10,000 is withdrawn and ₹8,000 is your principal, ₹2,000 is taxable as capital gains.

That makes SWP more tax-efficient than receiving dividends (which are taxed at slab rate).

🌍 SWP for Global Investors

Even global investors use Systematic Withdrawal Plans (SWPs) to generate cash flow from equity or balanced funds. The concept remains identical: periodic withdrawals from invested units.

For Non-Resident Indians (NRIs), SWPs are an excellent way to repatriate funds regularly to foreign bank accounts, subject to FEMA and RBI guidelines.

Always consult your tax advisor for cross-border taxation before initiating an SWP if you’re an NRI investor.

🧮 Example: SWP Calculation

Let’s visualize an SWP example:

- Investment: ₹10,00,000

- Monthly withdrawal: ₹15,000

- Fund return: 9% p.a.

| Year | Starting Balance | Withdrawal | Value End of Year | Remaining Balance |

|---|---|---|---|---|

| 1 | ₹10,00,000 | ₹1,80,000 | ₹10,27,000 | ₹8,47,000 |

| 2 | ₹8,47,000 | ₹1,80,000 | ₹8,55,000 | ₹6,75,000 |

| 3 | ₹6,75,000 | ₹1,80,000 | ₹6,80,000 | ₹5,00,000 |

| 4 | ₹5,00,000 | ₹1,80,000 | ₹5,08,000 | ₹3,28,000 |

| 5 | ₹3,28,000 | ₹1,80,000 | ₹3,30,000 | ₹1,50,000 |

Result → ₹7.5 lakh received in income, ₹1.5 lakh corpus remains.

🧠 SWP vs SIP: A Smart Combination

Many smart investors use SIP + SWP together:

- SIP for building wealth

- SWP for creating income later

You can start SIPs during your earning years and convert the same funds into SWPs when you retire or need cash flow.

This combination provides financial independence while keeping your money invested.

🎯 Final Thoughts

A Systematic Withdrawal Plan (SWP) is more than just a withdrawal option—it’s a financial strategy for smart investors who want consistent cash flow without stopping compounding.

It offers flexibility, tax efficiency, and control—three things every investor loves.

Whether you’re planning for retirement income, financial independence, or goal-based withdrawals, an SWP can be your best companion.

🪪 Need Personalized Guidance?

📞 Consult Omkar Mokashi, an AMFI-Registered Mutual Fund Distributor, via Busyshell to design a personalized SWP strategy aligned with your financial goals.

💬 Let your investments pay you every month—smartly and systematically!

🙋♀️ Frequently Asked Questions (FAQs)

1. What is an SWP in a mutual fund?

An SWP, or Systematic Withdrawal Plan, allows you to withdraw fixed amounts periodically while your remaining money stays invested.

2. Who should invest in an SWP?

Ideal for retirees, freelancers, or investors seeking steady income with capital growth potential.

3. Is SWP safe for regular income?

Yes, if done in balanced or debt funds; equity funds may have short-term volatility.

4. How is SWP different from dividends?

SWP withdrawals come from your own corpus, while dividends depend on fund performance and AMC policies.

5. Can I stop or modify my SWP?

Yes, you can start, pause, or change your SWP anytime—completely flexible.

6. What happens if NAV falls?

More units are redeemed when NAV decreases, but long-term performance tends to stabilize returns.

7. How is SWP taxed?

Only the gain portion of each withdrawal is taxed, making it more efficient than dividends.

8. Can NRIs use SWPs?

Yes, under FEMA and RBI rules, with repatriation possible through NRE/NRO accounts.

9. Is SWP available in all mutual funds?

Almost all open-ended mutual funds offer SWP options, both equity and debt.

10. Should I choose monthly or quarterly SWP?

Monthly is best for regular income; quarterly suits those with larger investment horizons.

⚠️ Disclaimer

This article is for educational purposes only and should not be construed as investment advice. Mutual fund investments are subject to market risks; read all scheme documents carefully before investing. Tax implications depend on individual circumstances and may change as per government regulations. For tailored advice, consult a certified financial or tax advisor.